点击蓝字 · 关注我们

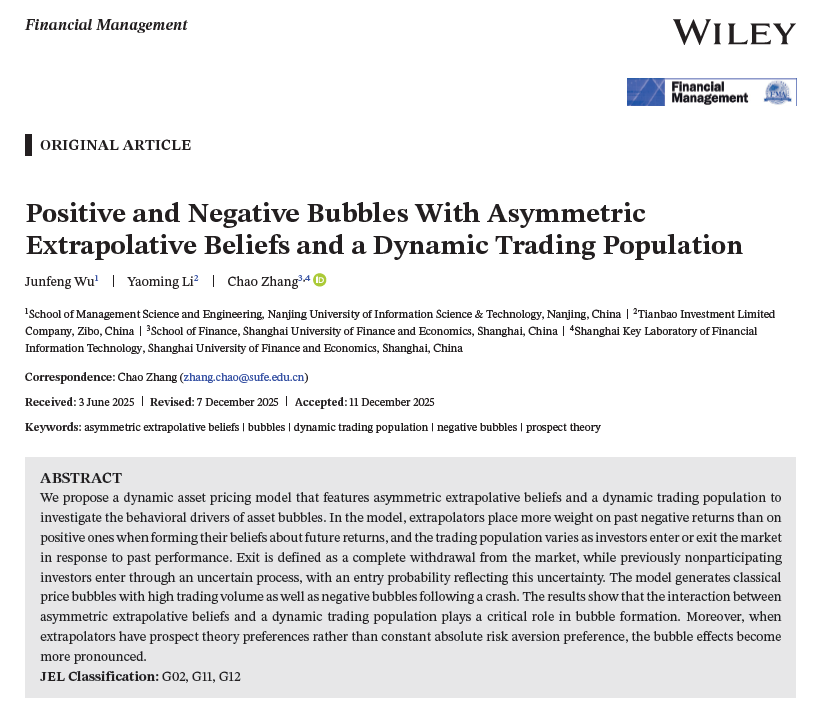

近期,我院张超老师与合作者的论文“Positive and Negative Bubbles With Asymmetric Extrapolative Beliefs and a Dynamic Trading Population”发表在国际权威期刊Financial Management上。在线资源请点击“阅读原文”获取链接。

论文简介

论文题目:Positive and Negative Bubbles with Asymmetric Extrapolative Beliefs and a Dynamic Trading Population

作 者: Junfeng Wu,Yaoming Li,Chao Zhang

发表杂志:Financial Management

英文摘要:

We propose a dynamic asset pricing model that features asymmetric extrapolative beliefs and a dynamic trading population to investigate the behavioral drivers of asset bubbles. In the model, extrapolators place more weight on past negative returns than on positive ones when forming their beliefs about future returns, and the trading population varies as investors enter or exit the market in response to past performance. Exit is defined as a complete withdrawal from the market, while previously nonparticipating investors enter through an uncertain process, with an entry probability reflecting this uncertainty. The model generates classical price bubbles with high trading volume as well as negative bubbles following a crash. The results show that the interaction between asymmetric extrapolative beliefs and a dynamic trading population plays a critical role in bubble formation. Moreover, when extrapolators have prospect theory preferences rather than constant absolute risk aversion preference, the bubble effects become more pronounced.

中文摘要:

本文构建了一个包含非对称外推信念与动态交易群体的资产定价动态模型,旨在探讨资产泡沫形成的行为驱动因素。在该模型中,外推型投资者在形成对未来收益的预期时,赋予过去负收益的权重高于正收益;同时,交易群体的规模会随投资者基于过往业绩的入市与退市行为而动态变化。我们定义“退市”为完全退出市场,而此前未参与交易的投资者则通过一个不确定性过程入市,入市概率用于描述该不确定性。模型不仅能够生成伴随高交易量的经典价格泡沫,还能够复现市场崩盘后出现的负泡沫。研究结果表明,非对称外推信念与动态交易群体的相互作用是推动泡沫形成的关键因素。此外,当外推型投资者的偏好遵循前景理论而非恒定绝对风险厌恶时,泡沫效应会更加显著。

期刊简介

Financial Management

Financial Management (FM) 是国际金融管理协会(FMA)的旗舰季刊,是财务管理领域的顶尖期刊之一,也是金融研究领域具有显著影响力和高质量研究的刊物。期刊主要发表关于金融市场、公司财务、资本结构、金融工程等方面的研究,涵盖理论与实证分析。近五年影响因子为4.8。

作者简介